Introduction

Most microfinance and localized credit businesses in Saudi Arabia are still run on chaotic WhatsApp threads, handwritten ledger notebooks, and memory. When a customer calls asking about their remaining installment, an agent has to manually flip through pages. When an investor asks how much profit their capital pool generated this month, there is rarely a clean, immediate answer ready.

Aman Credits decided to change all of that.

By building and operating a fully custom, Shariah-compliant credit management system, this business empowers administrators and branch dealers to seamlessly manage customer lifecycles, track investor pools, oversee tangible item inventory, and monitor multi-branch operations, all from a single digital dashboard screen.

This is a look at how that system works, what problems it solves, and why structured digital transformation is the future of ethical financing.

The Business Model — Smarter, Ethical, Item-Based Financing

Aman Credits does not operate like a standard conventional lending shop that issues cash loans. The platform operates on an interest-free, item-based financing framework that aligns with Islamic financial principles while scaling operational capability.

Tangible Asset Distribution (Interest-Free)

Unlike traditional lending platforms that revolve around interest-bearing transactions (which are prohibited under Islamic law), Aman Credits strictly provides financing through tangible items or goods. Customers apply for financing to purchase specific products rather than receiving monetary loans, completely eliminating interest-based friction.

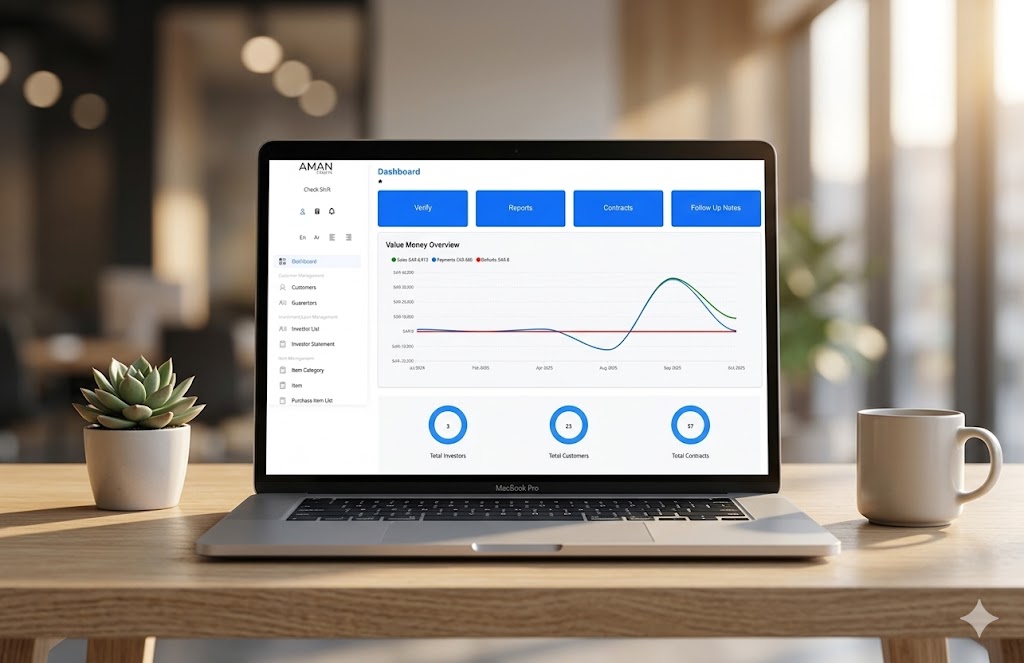

The Management System — Everything in One Place

At the core of this operation is a purpose-built, three-tier web admin ecosystem (built using React.js, Node.js, Express, and MySQL) that replaces manual paperwork and scattered communication.

Multi-Branch Visibility at a Glance

The centralized analytics dashboard gives the team real-time data visualization of the entire network. At any given second, management can monitor total active contracts, pending approvals, repayment statuses, and individual dealer records across independent branch locations.

Rigorous Customer Verification

Before a contract can even be drafted, the platform acts as a safeguard against defaults. Dealers use an automated identity verification screen to look up a customer’s valid identity number. The system checks if they are already registered and ensures they do not have active, overlapping debt contracts at any other branch in the network.

Risk-Controlled Guarantor Management

To back item-based contracts with legal and financial accountability, the system features a dedicated Guarantor Module. Dealers can effortlessly register and link one or multiple verified guarantors to a customer’s profile, validating identity details to ensure no single guarantor exceeds system-defined support limits.

Inventory & Purchase Item Logistics

Because credit is asset-based, tracking inventory is critical. The system manages full inventory categories (e.g., electronics, home appliances) across branches. It tracks original purchase costs, monitors remaining stock levels, and locks approved goods directly to customer files during contract creation.

Clean Investor Statements

With multiple investors contributing capital, transparency is paramount. The system tracks every deposit, withdrawal, and transaction log per investor. It outputs clean, real-time Investor Statements, completely eliminating end-of-month payout confusion.

The Financial Picture — Absolute Compliance & Control

One of the most powerful features of Aman Credits is its uncompromising data governance and accounting control. By building the backend with custom-written SQL queries instead of an abstract ORM, the platform manages high-volume financial calculations instantly and accurately.

At any given moment, the business has absolute clarity over:

- The "Value Money Overview": A dynamic visual graph displaying total investments, distributed credits, repayments, and outstanding balances.

- Secure Shift Operations: Daily branch transactions are isolated into strict shift sessions. Dealers open and close shift sessions, creating logged daily transaction summaries that prevent cash-flow leakage.

- Granular Receipts & Settlements: Every installment payment generates an instant, verifiable digital Receipt that recalculates the remaining balance automatically until a final Contract Completed legal settlement is outputted.

Why This Approach Changes the Industry

Traditional microfinance operations have historically struggled with critical operational blind spots:

- Paperwork & Disorganization: Relying on physical folders or unorganized records causes expensive tracking errors.

- Interest Limitations: Businesses want to offer ethical credit, but manual tracking makes asset-based financing too complex to execute at scale.

- Trust Deficits: Investors walk away when there are no clear logs detailing how their pooled funds are being used.

Aman Credits solves these exact pain points by modularizing the entire operation. It turns an ethical compliance challenge into a structured, highly scalable, and repeatable digital process.

What the System Makes Possible

- Onboard independent dealers and assign structured branch permissions with total administrative control.

- Enforce Dealer Light Mode to instantly simplify the UI and hide advanced operational features in fast-paced retail branches.

- Ensure strict Shariah compliance by anchoring every credit agreement to verified, tangible items.

- Generate actionable analytical reports cards across sales, collections, and defaults with a modular grid interface.

- Drive sustainable growth in Islamic microfinance without the admin overhead.

Conclusion

The gap between a chaotic credit operation and a thriving, ethical microfinance network comes down to having the right systems. When you can instantly verify a customer's identity, pull up an unalterable contract, audit an investor pool, and review daily shift totals from a single web interface, you stop firefighting and start expanding.

Aman Credits is living proof that combining rigorous faith-based ethics with a modern, data-driven full-stack architecture is the ultimate trajectory for modern financial management systems.